Patient Lateral Transfer Devices Market To Witness High Growth Owing To Rising Geriatric Population11/30/2023  Patient Lateral Transfer Devices Market The Patient Lateral Transfer Devices market is estimated to be valued at US$ 350.91 Mn in 2023 and is expected to exhibit a CAGR of 9.7% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Patient lateral transfer devices are used to safely transfer patients from one surface to another like beds, stretchers, wheelchairs etc. These devices are designed to provide comfort, stability and safety to patients during transfer. Lateral transfer devices help to reduce the risk of injury to caregivers during the transfer process. Common lateral transfer devices include sliding sheets/boards, transfer/evacuation mattresses, blankets, air assisted mattresses and related accessories. Market Dynamics: The growth of the patient lateral transfer devices market is majorly driven by the rising geriatric population globally which is more prone to disabilities and medical conditions requiring assistance in movement and transfer. As per United Nations report, by 2050 around 16.9% of the global population will be aged 65 years and above. This growing pool of geriatric population will propel the demand for these devices from hospitals and long term care facilities. Additionally, increasing incidence of chronic diseases such as orthopedic disabilities, obesity and paralysis are leading to rising hospital admissions and need for lateral transfer of patients from beds to stretchers and vice versa, further fueling market growth over the forecast period. However, high costs associated with powered and air assisted lateral transfer devices may restrain market growth to some extent. SWOT Analysis Strength: Patient Lateral Transfer Devices help in safe transfer of patients from one surface to another and reduce manual handling induced injuries to caregivers. These devices are equipped with sliding sheets and rails for easy maneuverability. They are available in wide range of designs to suit varied patient conditions. Weakness: High cost associated with advanced Patient Lateral Transfer Devices limits their adoption in budget constrained settings. Lack of training to caregivers can lead to device misuse and patient safety issues. Opportunity: Growing geriatric population and rising healthcare expenditure in developing nations create demand. Development of tech-enabled devices for bariatric, pediatric and disabled patients present new areas of growth. Threats: Preference for alternate handling equipment and lifting solutions by some hospitals. Stringent regulatory approval process and quality standards delay product launches. Key Takeaways Global Patient Lateral Transfer Devices Market Demand is expected to witness high growth, exhibiting CAGR of 9.7% over the forecast period, due to increasing prevalence of chronic diseases and mobility issues among aging population. Regional analysis: North America dominates the global market owing to rising health awareness, availability of advanced medical technologies and significant per capita healthcare spending in the US and Canada. The Asia Pacific region is expected to exhibit fastest growth due to growing medical tourism, rising income levels and expansion of private healthcare sector in China, India and Southeast Asian countries. Key players: Key players operating in the Patient Lateral Transfer Devices market are Stryker Corporation, Hill-Rom Holdings Inc., Arjo, Handicare AB, Etac AB, Sizewise, McAuley Medical Inc., Medline Industries Inc., Samarit Medical AG, Blue Chip Medical, Haines Medical Australia, Scan Medical Co Inc., Wy'East Medical, GBUK Banana, AliMed Inc., Cantel Medical Corporation, EZ Way Inc., and Patient Positioning Systems LLC. Read More- https://www.ukwebwire.com/patient-lateral-transfer-devices-market-size-share-and-demand-outlook/

0 Comments

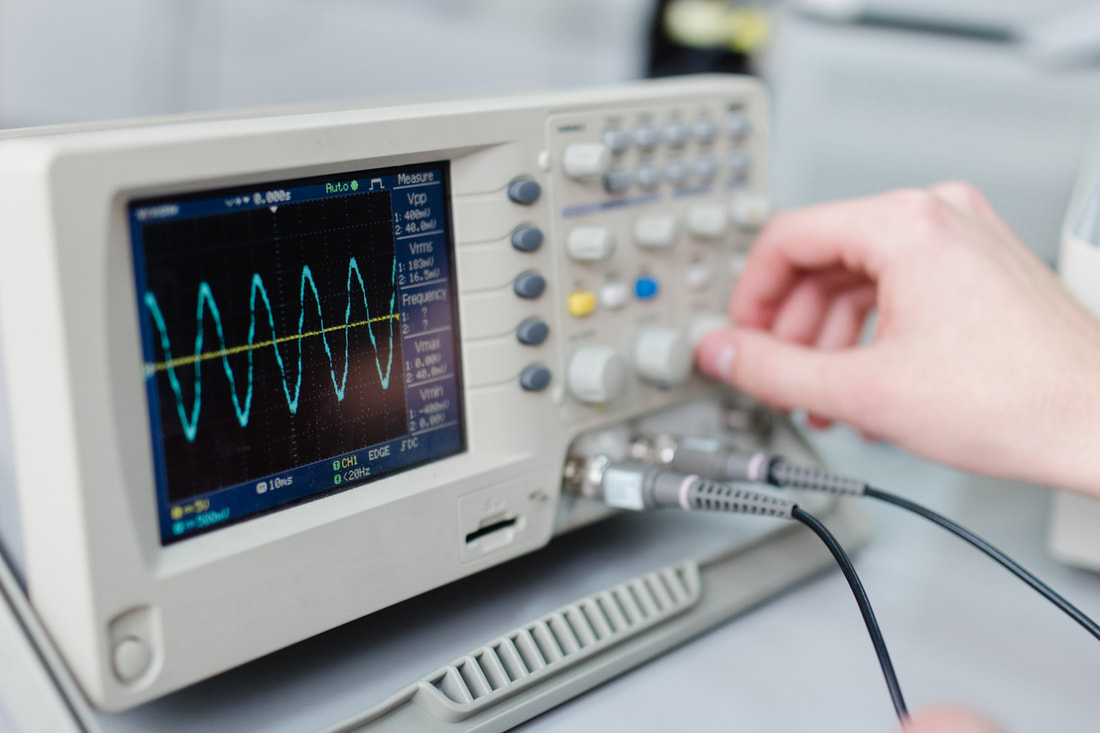

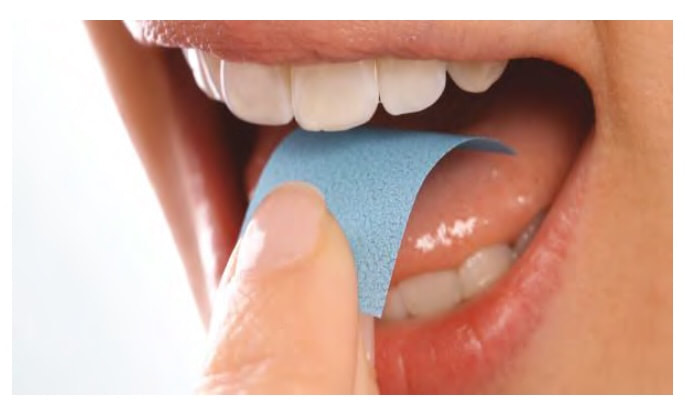

Partner Relationship Management Solution Market The Partner Relationship Management Solution market is estimated to be valued at US$ 17760.06 Mn in 2023 and is expected to exhibit a CAGR of 18% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview Partner relationship management (PRM) solutions help organizations and companies manage relationships with channel partners, distribution partners, and other external stakeholders. These solutions empower organizations to streamline partner onboarding, optimize partner communication and collaboration, track performance metrics, facilitate payments and commissions, provide dedicated partner portals for resources and training. PRM solutions enhance visibility into partner activities, improve engagement through centralized information & workspace, and help maximize revenue through partners. Market Dynamics The growth of the Partner Relationship Management Solution market is propelled by growing need to optimize partner engagement and drive revenue growth through channel partners and external stakeholders. PRM solutions enable organizations to onboard and manage high volumes of partners, track partner activities in real-time, facilitate program design and performance-based incentives, and provide analytical insights to improve partner communication and strategy. Additionally, PRM solutions facilitate seamless partner management across geographical boundaries in a cost-effective manner, which is another factor boosting their adoption. SWOT Analysis Strength: Partner Relationship Management Solution helps companies streamline partner engagement and operations. It provides real-time visibility into partner activities and performance. It also offers automated workflows and role-based access control for improved collaboration. Weakness: Implementing a PRM solution requires significant investments and resources. It also needs careful change management to adapt employees to new processes. Data migration from legacy systems can also be challenging. Opportunity: Growing demand for enhancing partner experience and optimizing partner relationships. Adoption of cloud-based solutions is also creating opportunities for vendors. Rising focus on digital transformation of partner programs will drive the market. Threats: Competition from open-source and freemium PRM tools. Rising concerns around data privacy and security can impact market growth. Key Takeaways Global Partner Relationship Management Solution Market Size is expected to witness high growth, exhibiting CAGR of 18% over the forecast period, due to increasing demand for centralized partner management and optimized partner engagement strategies. Regional analysis: North America is expected to dominate the PRM solution market during the forecast period. Growing adoption of cloud-based solutions among enterprises is driving the market in the region. The Asia Pacific region is expected to exhibit the fastest growth due to rapid digital transformation of partner ecosystems in countries like China and India. Key players: Key players operating in the Partner Relationship Management Solution market are Salesforce.com, Inc., LogicBay Corporation, Oracle Corporation, Allbound Inc., International Business Machines Corp, Impartner Software, ZINFI Technologies, Inc., Zyme Solutions, PartnerPath, Blackhawk Engagement Solutions, Inc., The Planet Group, Allbound Inc., and Channeltivity, LLC. These players are focusing on enhancing their cloud-based offerings and partner experience management capabilities. Read More- https://www.ukwebwire.com/partner-relationship-management-solution-market-demand-analysis-and-insights/  Oscilloscope Market The oscilloscope market is estimated to be valued at US$ 2311.04 Mn in 2023 and is expected to exhibit a CAGR of 5.1% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: An oscilloscope is an electronic test instrument used to measure, graph and display electrical signals including voltages and currents over time. It digitizes, graphically plots and analyzes a signal in real-time for detection of noise, non-periodic signals and frequency components. Oscilloscopes are used extensively by electrical and electronics engineers to debug electronic circuits, analyze signal integrity issues, measure signal slew rate, distortion, rise and fall time and peak-to-peak voltages. Modern digital oscilloscopes provide higher measurement accuracy and bandwidths up to 3GHz with compact form factors for applications in design verification, manufacturing, quality testing and troubleshooting. Market Dynamics: Rising adoption of digital oscilloscopes over analog oscilloscopes across industries drives market growth. Digital oscilloscopes provide higher accuracy, greater bandwidths up to 3GHz and flexible triggering facilities. They digitize and mathematically process the analog input signals to display crisp waveforms on high-resolution color displays. Additionally, growing demand for oscilloscopes in the consumer electronics manufacturing and automotive sectors for verifying circuit designs and performing production tests also augments market expansion over the forecast period. Furthermore, introduction of more advanced features such as built-in digital multimeters and high sampling rates up to 5Giga sample per second in modern oscilloscopes facilitates capturing low-amplitude signals and analysis of high-speed circuits. However, availability of free open-source oscilloscope software applications poses a challenge for established oscilloscope manufacturers. SWOT Analysis Strength: Oscilloscope have wide application in electronic industry for testing and measurement which leads to consistent demand. Presence of major players providing quality products expand market reach. Technological advancement leads to compact size and higher bandwidth oscilloscopes. Weakness: High cost of modern oscilloscopes limits adoption among small testing labs and industries. Skill requirement for operating advanced oscilloscopes may lead to improper usage. Opportunity: Growth of wearable devices and IoT ecosystem accelerates demand for portable oscilloscopes. Rising electronics exports from developing countries creates new sales opportunity. Customized oscilloscopes for specialized applications present an untapped sector. Threats: Availability of pre-owned and refurbished oscilloscopes at lower cost threatens new equipment sales. Slowdown in electronics manufacturing during economic recession affects oscilloscope demand. Key Takeaways Global Oscilloscope Market Size is expected to witness high growth, exhibiting CAGR of 5.1% over the forecast period, due to increasing demand for testing and debugging electronic devices. The market size for 2023 is US$ 2311.04 Mn. Regional analysis: North America dominated the oscilloscope market in 2021 with highest share of over 30%, owing to wide presence of electronics manufacturing facilities in the US and Canada. Asia Pacific is anticipated to witness fastest growth during the forecast period supported by increasing electronics exports from China, India, Taiwan and South Korea. Key players analysis: Key players operating in the oscilloscope market are Scientech Technologies Pvt. Ltd., Tektronix Inc., B&K Precision Corporation, Keysight Technologies Inc., Pico Technology Holdings Ltd., Rohde & Schwarz GmbH & Co. KG, Siglent Technologies Co. Ltd., Teledyne LeCroy Inc., Fluke Corporation, Yokogawa Test & Measurement Corporation, Rigol Technologies Inc., and National Instruments Corporation. These players are focusing on new product launches and expansions to strengthen their global presence. Read More- https://www.ukwebwire.com/oscilloscope-market-size-share-and-demand-insights/ Oral Thin Films are Estimated To Witness High Growth Owing To Increased Patient Compliance11/30/2023  Oral Thin Films Market 'The oral thin films market is estimated to be valued at US$ 2,895.55 Mn in 2023 and is expected to exhibit a CAGR of 8.7% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights.

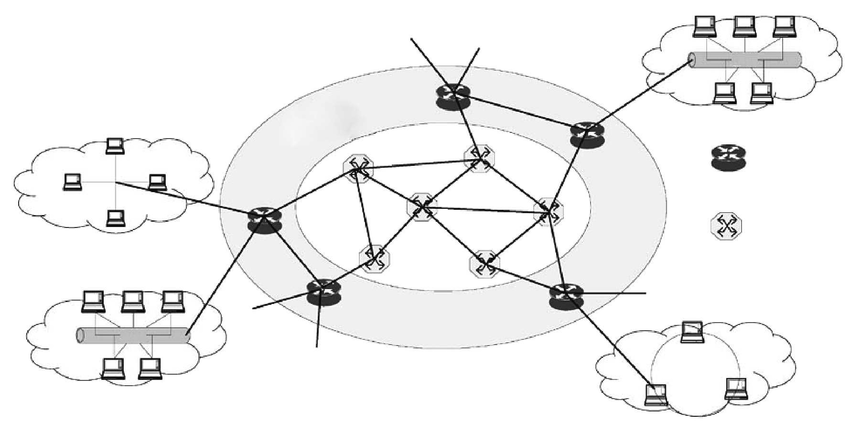

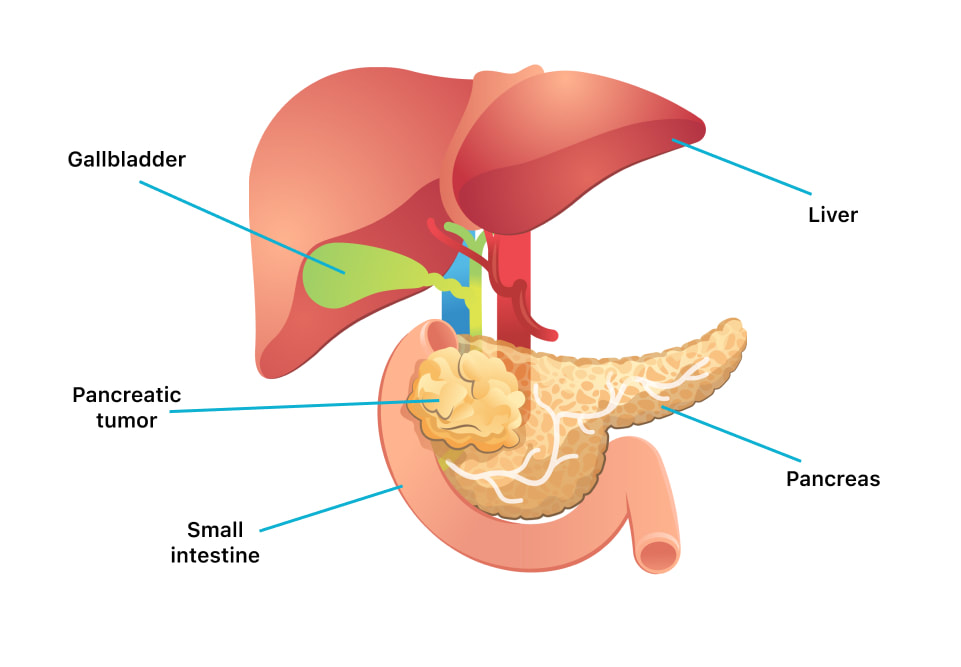

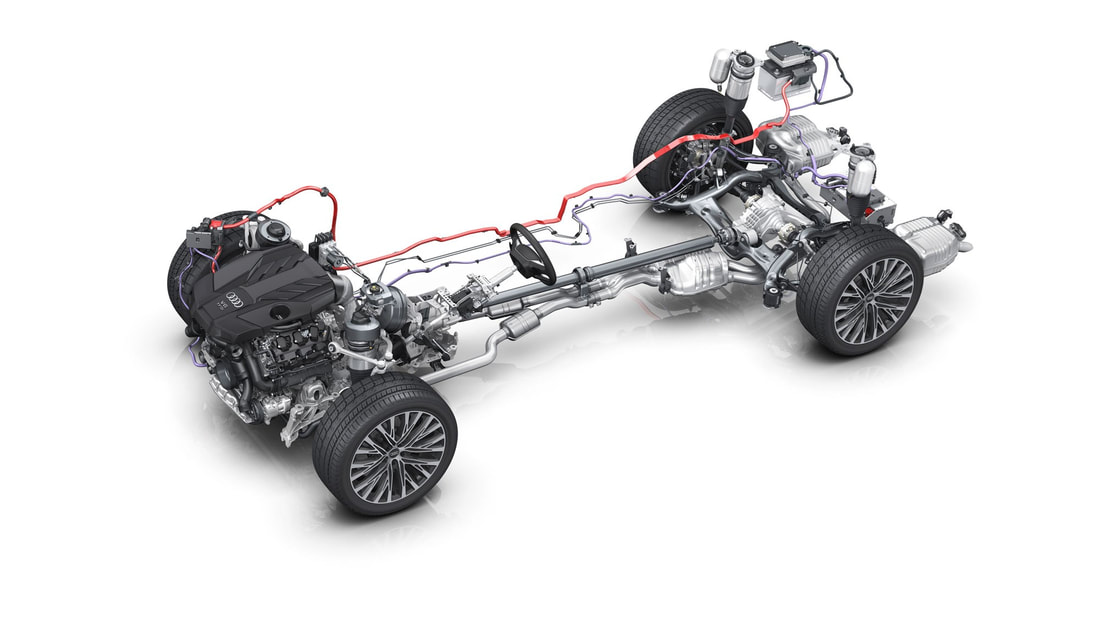

Market Overview: Oral thin films are medicated film formulated to dissolve rapidly in the mouth. The consumption of oral thin films provides rapid drug release and absorption compared to tablets or capsules. Oral thin films are commonly used for various therapeutic applications including motion sickness, migraine, cold & cough, erectile dysfunction, and smoking cessation. Key advantages of oral thin films include easy administration, minimal or no water requirement, and improved patient compliance especially for pediatric and geriatric population compared to tablets and capsules. Market Dynamics: Growing patient preference for easy and convenient dosage forms is expected to drive the growth of oral thin films market over the forecast period. Oral thin films are easier to administer over conventional tablets and capsules as they dissolve in the mouth without water. This provides rapid action and enhances patient compliance especially for pediatric and geriatric population. Moreover, oral thin films exhibit manufacturing flexibility to incorporate various molecules for developing combination products. This is further expected to fuel the adoption of oral thin films. Rising geriatric population also plays a key role as elderly patients prefer oral thin films over other dosage forms due to problems in swallowing. However, limited drug loading capacity of oral thin films acts as a major restraining factor. SWOT Analysis Strength: Oral thin films have three key strengths - they are convenient to administer, rapidly dissolve in the mouth without water, and have improved bioavailability compared to tablets. Their compactness and portability make them ideal for on-the-go usage. They also improve patient compliance as medicines can be discreetly taken. Weakness: High manufacturing costs and shorter shelf life are two weaknesses of oral thin films. Producing a uniform thin film requires specialized equipment and technology which increases production costs. Their thinness also makes them vulnerable to damage from moisture during storage and transportation. Opportunity: Growing preference for alternative drug delivery formats and expanding applications present opportunities. Patients increasingly prefer convenient dosage forms, boosting demand for oral thin films. Their usage is expanding beyond applications in neurology and into new therapeutic areas like cardiology, which can drive future growth. Threats: Stringent regulatory norms and competition from existing drugs are threats. Regulatory standards for film manufacturing are complex, raising entry barriers. Established drugs like tablets also compete for shares, posing commercialization challenges. Dependence on a limited number of suppliers for raw materials is another threat. Key Takeaways Global Oral Thin Films Market Demand is expected to witness high growth, exhibiting CAGR of 8.7% over the forecast period, due to increasing preference for alternative drug delivery formats. Rapidly dissolving oral thin films offer convenience over traditional tablets for patients. Regional analysis: North America is currently the dominant regional market for oral thin films, accounting for over 35% revenue share in 2023. However, Asia Pacific is expected to witness fastest growth owing to rising healthcare spending and growing patient demand in populous nations like China and India. Key players: Key players operating in the oral thin films market are C L Pharm, Cure Pharmaceutical, Sunovion Pharmaceuticals Inc., ZIM Laboratories Limited, NAL Pharma, Viatris, LTS Lohmann Therapie-Systeme AG, IntelGenx Corp., and Aquestive Therapeutics Inc., among others. These players are focusing on new film formulations and expanding applications beyond current neurology and smoking cessation usages. read more- https://www.ukwebwire.com/oral-thin-films-market-value-inisghts-and-forecast/  Optical Transport Network Market The Optical Transport Network market is estimated to be valued at US$ 22.32 Bn in 2023 and is expected to exhibit a CAGR of 10 % over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: An optical transport network (OTN) allows the transmission of digital signals between different network segments with help of wavelength multiplexing technology. It provides end-to-end networking capabilities for services as it combines the functions of packet transport, optical routing, wavelength switching and optical cross-connection into a single highly scalable network. Using dense wavelength-division multiplexing (DWDM), it transmits multiple signals simultaneously over the same fiber. Products in the OTN market include WDM, optical switches, optical packet switches and others, which are used by telecom service providers for infrastructure modernization, bandwidth-intensive services and IP-centric networks. Market Dynamics: The growth of the optical transport network market is driven by growing demand for high-speed data delivery to support data-intensive applications such as cloud computing, internet of things, video streaming, virtual/augmented reality. According to Cisco, global IP traffic will reach 4.8 zettabytes per year by 2022, up from 1.5 zettabytes in 2017. This rising traffic demand is prompting network operators to upgrade copper-based networks to fiber connections and adopt technologies like OTN. Also, increasing adoption of 5G networks globally will augment the need for robust transport infrastructure, fueling market growth over the forecast period. However, high initial infrastructure costs associated with optical networks may restrain market growth. SWOT Analysis Strength: - High bandwidth and scalability of optical transport networks allows high data transfer speeds. - Optical fibers provide reliable and secure transmission with least interference. - OTN helps in effective utilization of fiber bandwidth through efficient networking protocols. Weakness: - Initial investment required for setting up the optical infrastructure is very high. - Lack of trained workforce for operating and maintaining the OTN equipment. Opportunity: - Increasing mobile data traffic and popularity of technologies like 5G, IoT and cloud computing is boosting the demand for optical transport networks. - Optical components and solutions are evolving to offer higher scalability, reliability and efficiency to support future bandwidth needs. Threats: - Stiff competition among existing players can lead to pricing pressures. - Cyclical nature of capital expenditure in the telecom sector may impact market revenues. Key Takeaways Global Optical Transport Network Market Size is expected to witness high growth, exhibiting CAGR of 10% over the forecast period, due to increasing mobile data traffic and roll out of 5G networks worldwide. Major telecom operators are upgrading their transport infrastructure to higher speed networks to support growing data demand. Regional analysis Asia Pacific dominates the global optical transport network market with over 35% share, led by heavy investments in broadband and mobile infrastructure in countries like China, India. Rapid technological adoptions and expanding subscriber base are driving the demand. North America and Europe hold significant shares owing to widespread coverage of high-speed networks. Key players Key players operating in the optical transport network market are Nokia Corporation, Ciena Corporation, Cisco Systems Inc., Huawei Technologies Co. Ltd, ZTE Corporation, Fujitsu Corporation, Infinera Corporation, Telefonaktiebolaget LM Ericsson, NEC Corporation and Yokogawa Electric Corporation. Market leaders are focusing on developing solutions with enhanced capabilities to strengthen their positions. Read More- https://www.ukwebwire.com/optical-transport-network-market-size-share-and-value-insights/  Operating Tables and Lights Market The operating tables and lights market is estimated to be valued at US$ 1491.9 Mn in 2023 and is expected to exhibit a CAGR of 3.9% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: The operating tables and lights market comprises of medical equipment used in operating rooms for surgical procedures. Operating tables are designed for positioning, manipulating and securing patients for surgical procedures, while operating lights or surgical lights provide illumination for surgical procedures by concentrating light in the operating field. Operating tables and lights are used in various surgical procedures such as spine surgeries, orthopedic surgeries, ENT surgeries, neurosurgeries, cardiothoracic surgeries and general surgery. Market Dynamics: The operating tables and lights market is witnessing growth owing to rising number of surgical procedures globally. According to the American Society of Plastic Surgeons, around 18.1 million surgical and minimally-invasive cosmetic procedures were performed in the U.S. in 2019. Growing prevalence of chronic diseases such as cardiovascular diseases, cancer, diabetes and dental diseases is also fueling market growth. Moreover, technological advancements in operating tables introducing features such as adjustable positions and motorized controls for positioning are gaining popularity in operating rooms. However, high costs associated with modern operating tables and lights, and budget constraints in hospitals of developing economies, may hamper market growth. SWOT Analysis Strength: Operating tables and lights market has strong presence of key players with wide product portfolio. Advanced features such as movable monitors and integrated lights provide better ergonomics and convenience to surgeons. Rising demand for minimally invasive surgeries drives the growth of this market. Weakness: High cost of advanced operating tables poses affordability challenges in price sensitive areas. Lack of proper training to operate advanced features limits full utilization of potential. Opportunity: Emerging markets in Asia Pacific provide huge untapped growth opportunities due to rising healthcare investments and infrastructure. Increasing number of ambulatory surgical centers augment the demand for operating tables and lights. Threats: Currency fluctuations and trade wars impact profit margins of global players. Slow hospital spending and delays in capital expenditures impact new installations. Key Takeaways Global Operating Tables And Lights Market Demand is expected to witness high growth, exhibiting CAGR of 3.9% over the forecast period, due to increasing number of surgical procedures worldwide. The market size was valued at US$ 1491.9 Mn in 2023. Regional analysis The Asia Pacific region is expected to grow at the fastest rate due to rising healthcare infrastructure, presence of low cost manufacturing bases, and increasing healthcare spending. China, India and Japan dominate the Asia Pacific operating tables and lights market with largest patient pools. North America accounted for the largest revenue share in 2023 led by technological advancements, higher adoption of advanced medical devices and large number of ambulatory surgical centers in the US and Canada. Key players Key players operating in the operating tables and lights market are Siemens AG, Dragerwerk AG & Co. KGaA, Getinge AB, GE Healthcare, Hill-Rom Holdings, Inc., KARL STORZ GmbH & Co. KG, Mizuho OSI, Koninklijke Philips N.V., STERIS Corporation, Stryker Corporation, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., BenQ Medical Technology, Mediland Enterprise Corporation, Alvo Medical Sp. z o.o., Famed Zywiec Sp. z o.o., Heal Force, OPT Surgisystems S.R.L. (TKB Group), Medifa-hesse GmbH & Co. KG, UFSK-International OSYS GmbH, Taicang Kanghui Technology Development Co., Ltd, Ningbo Techart Medical Equipment Co., Ltd., Fazzini SRL, Lojer Oy, and AGA Sanitaetsartikel GmbH. The key players are focusing on new product launches and geographical expansion to gain higher market share.  Oncology Radiopharmaceuticals Market The Oncology Radiopharmaceuticals market is estimated to be valued at US$ 7351 Mn in 2023 and is expected to exhibit a CAGR of 45.% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. The oncology radiopharmaceuticals market is witnessing high growth owing to the increasing incidence of cancer across the globe. According to the World Health Organization (WHO), cancer was responsible for nearly 10 million deaths in 2020. The four most common types of cancer in 2020 were lung cancer, breast cancer, colon and rectal cancer, and prostate cancer. As per the National Cancer Institute, in the U.S., approximately 1.8 million new cancer cases and 606,520 cancer deaths are projected to occur in 2022. Thus, the rising prevalence of cancer is expected to drive the demand for effective diagnostic and therapeutic procedures for cancer detection and treatment over the forecast period. Market Overview Oncology radiopharmaceuticals are radioactive compounds used for both diagnosis and treatment of cancer. PET and SPECT radiotracers containing short-lived radioactive isotopes are being used widely for cancer imaging, targeting tumors and evaluating cancer therapies. Radioisotopes such as Fluorine-18, Technetium-99m, Iodine-123, Iodine-131, Gallium-67 and Indium-111 help in localization and visualization of tumors and thus play a critical role in staging, restaging and monitoring cancer. Radionuclides emitting therapeutic radiation are also being used to treat various cancers such as thyroid cancer, bone cancer, lymphoma etc. The oncology radiopharmaceuticals market offers various products such as SPECT radiopharmaceuticals and PET radiopharmaceuticals which find applications in tumor localization and cancer theranostics. Market Dynamics The growing adoption of PET and hybrid imaging techniques such as PET/CT and PET/MRI for cancer diagnosis and monitoring responses to therapy is fueling market growth. PET offers higher sensitivity for cancer detection as compared to conventional imaging techniques. Furthermore, advantages such as minimal invasion, cost-effectiveness and ability to frequently image tumors are increasing PET adoption in radiology oncology practices. Efforts towards development of new radioisotopes and radiotracers as well targeted SWOT Analysis Strength: The oncology radiopharmaceuticals market experiences strong growth due to the rising preference for precision medicine and targeted radiotherapy among oncologists. Radiopharmaceuticals help diagnose and treat cancer more accurately. The market witnesses numerous product approvals and launches each year to fulfill the increasing demand. Weakness: High costs associated with research and development of novel radiopharmaceuticals hamper market growth. Many countries lack skilled professionals to produce and use radiopharmaceuticals efficiently. Opportunity: Untapped potential in emerging economies provides lucrative opportunities for market players. Growing geriatric population prone to cancer augments demand. Threats: Stringent regulatory frameworks for approval delay market access. Supply chain disruptions amid the ongoing pandemic pose challenges. Key Takeaways Global Oncology Radiopharmaceuticals Market Demand is expected to witness high growth, exhibiting CAGR of 45% over the forecast period, due to increasing cancer prevalence worldwide. Growing adoption of nuclear medicine for cancer diagnostics and therapeutics boosts market revenue. Regional analysis: North America dominates the oncology radiopharmaceuticals market and is expected to retain its leading position during the forecast period. High healthcare spending and advanced healthcare infrastructure support market growth. Asia Pacific exhibits the fastest growth attributed to rising healthcare awareness, healthcare reforms, and increasing cancer burden in China and India. Key players operating in the oncology radiopharmaceuticals market are Siemens Healthcare GmbH, Novartis AG, Curium, GE Healthcare, Lantheus Medical Imaging, Inc., International Isotopes, Inc., Nordion, Eckert & Zieger, Acrotech Biopharma, Blue Earth Diagnostics, Zionexa, Bayer AG, Jubilant Pharma Limited, and Cardinal Health. Key players are involved in frequent new product launches and collaborations for sustained market shares. Read More- https://www.ukwebwire.com/oncology-radiopharmaceuticals-market-forecast-analysis-and-outlook/  Nausea Medicine Market The nausea medicine market is estimated to be valued at US$ 7.52 Bn or Mn in 2023 and is expected to exhibit a CAGR of 5.9% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Nausea medicines are used to treat nausea and vomiting associated with gastrointestinal disorders, cancer treatment (chemotherapy), and pregnancy. The main product types include antacids, antiemetics, anticholinergics and antihistamines. Antacids are commonly used to treat nausea associated with indigestion and acidity, while antiemetics work specifically on nausea and vomiting. Market Dynamics: Increasing prevalence of gastrointestinal disorders such as motion sickness, gastroenteritis and acid reflux is expected to drive growth of the nausea medicine market. According to the American Gastroenterological Association, around 60-70 million people in the US are affected by acid reflux or GERD annually. Moreover, rising cancer cases and growing demand for effective antiemetic drugs for chemotherapy-induced nausea and vomiting will also contribute to market growth. However, side effects associated with long term usage of nausea medicines and preference for alternative therapies may hamper the market to a certain extent over the forecast period. SWOT Analysis Strength: A growing awareness of nausea and its effective treatment among consumers is driving growth of this market. Also, advancement in drug delivery methods like extended release formulations makes these medicines more effective. Presence of established players with strong distribution networks further aid market growth. Weakness: High development and regulatory costs associated with drug development is a weakness for small players in this space. Side effects of some nausea medicines reduces patient compliance. Opportunity: Emergence of innovative drug formulations and delivery methods presents an opportunity for players. Also, a rising elderly population which is more susceptible to nausea related conditions will augment demand. Threats: Expiry of patents opens up the market for generic competitors. Stringent regulatory processes for new drug approvals can delay market entry for players. Key Takeaways Global Nausea Medicine Market Demand is expected to witness high growth, exhibiting CAGR of 5.9% over the forecast period, due to increasing prevalence of nausea inducing conditions like motion sickness, gastrointestinal disorders, chemotherapy, and post-surgery effects. Regional analysis: North America dominates the global nausea medicine market currently. This is attributed to the presence of affluent consumers and advanced healthcare infrastructure in the region. Asia Pacific is expected to be the fastest growing market owing to rising healthcare spending and increasing awareness about disease conditions treated by these medicines. Key players: Key players operating in the nausea medicine market are GlaxoSmithKline plc, Pfizer Inc., Novartis International AG, Sanofi S.A., Merck & Co., Inc., Johnson & Johnson, Bayer AG, Takeda Pharmaceutical Company Limited, AstraZeneca plc, Eli Lilly and Company. These players are focused on developing novel formulations to strengthen their product portfolios.  Pancreatic Cancer Therapeutics and Diagnostic Market The pancreatic cancer therapeutics and diagnostic market is estimated to be valued at US$ 4255.87 Mn in 2023 and is expected to exhibit a CAGR of 7.4% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: The pancreatic cancer therapeutics and diagnostic market consists of therapies used for treatment and diagnosis of pancreatic cancer. The various products available in the market include drugs, imaging equipment and reagents & kits. Therapies primarily include chemotherapy, immunotherapy and targeted therapy. Imaging modalities used for diagnosis include endoscopic ultrasound, CT scan, MRI etc. Biopsy and tumor marker tests are also conducted to diagnose pancreatic cancer. Market Dynamics: The pancreatic cancer therapeutics and diagnostic market is primarily driven by rising incidence of pancreatic cancer globally. According to the National Cancer Institute, it is estimated that around 60,430 Americans will be diagnosed with pancreatic cancer in 2022. Other key drivers include growing geriatric population, increasing adoption of imaging modalities for diagnosis and rising number of clinical trials evaluating efficacy of novel drugs. However, poor prognosis of the disease coupled with limited treatment options continues to restrain the market growth. High cost of therapies and risk of adverse effects also challenges the market. Innovation in imaging technologies and development of targeted and immuno-oncology drugs are expected to provide lucrative opportunities over the forecast period. SWOT Analysis Strength: - Increasing research and development activities for developing advanced therapeutics and diagnostics. - Rising adoption of targeted therapy and immunotherapies for pancreatic cancer treatment. - Growing awareness regarding pancreatic cancer and available treatment options. Weakness: - Late diagnosis of pancreatic cancer hampers successful treatment. - High cost associated with pancreatic cancer therapeutics and diagnostic procedures limits accessibility. Opportunity: - Untapped emerging markets present lucrative opportunities for market expansion. - Development of novel early detection techniques can increase survival rate of patients. Threats: - Stringent regulatory framework for approval of pancreatic cancer drugs increases complexity. - Alternative treatment options pose threat to market growth. Key Takeaways Global Pancreatic Cancer Therapeutics And Diagnostic Market Size is expected to witness high growth, exhibiting CAGR of 7.4% over the forecast period, due to increasing incidence of pancreatic cancer worldwide. Regional analysis: North America dominates the market and is expected to continue its dominance over the forecast period. This is attributed to growing elderly population, increasing healthcare spending, and high adoption of advanced treatment in the region. Asia Pacific exhibits the fastest growth due to rising awareness, improving healthcare infrastructure, and expanding patient pool. Key players: Key players operating in the Pancreatic Cancer Therapeutics And Diagnostic market are F. Hoffmann-La Roche AG, Merck KGaA, Apexigen Inc., Immunovia AB, Viatris Inc., Amgen Inc., AstraZeneca PLC, Bristol-Myers Squibb, Novartis AG, Pfizer Inc., Myriad Genetics Inc., Canon Medical Systems Corporation, FUJIFILM Holdings Corporation, Boston Scientific Corporation, and Rafael Holdings Inc. (Rafael Pharmaceuticals), among others. Read More- https://www.trendingwebwire.com/pancreatic-cancer-therapeutics-and-diagnostic-market-growth/  Mild Hybrid Vehicle Market The mild hybrid vehicle market is estimated to be valued at US$ 99.97 Bn in 2023 and is expected to exhibit a CAGR of 18.% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview Mild hybrid vehicles use a combination of an internal combustion engine along with an integrated starter generator (ISG) system and a small battery for power assistance during acceleration and braking. The ISG system provides power boost during acceleration and recovers energy during braking which helps in improving fuel efficiency. Mild hybrid vehicles are primarily used for short city or suburban trips which see frequent starts and stops. They provide 10-15% better fuel efficiency compared to conventional vehicles. Market Dynamics The global mild hybrid vehicle market is driven by rising demand for fuel efficient vehicles. Stringent emission norms by regulatory bodies worldwide are putting pressure on automakers to reduce carbon footprint of vehicles. Mild hybrid systems help automakers comply with emission norms in a cost effective way. Additionally, improving charging infrastructure is also fueling the adoption of mild hybrid electric vehicles. Growing consumer awareness about environmental impact of conventional vehicles is another key factor pushing the uptake of hybrid electric vehicles including mild hybrid variants. Rebates and tax benefits offered by governments in various countries on purchase of electric vehicles including mild hybrids is also augmenting the market growth. However, high manufacturing cost of hybrid systems and availability of cheaper conventional powertrains continue to restrict broader adoption of mild hybrid vehicles. SWOT Analysis Strength: Mild hybrid vehicles provide improved fuel efficiency compared to conventional vehicles which help reduce fuel costs. They offer enhanced acceleration and power compared to regular vehicles. Mild hybrid vehicles also help reduce vehicular emissions and comply with stringent emission regulations. Weakness: The initial costs of mild hybrid vehicles are slightly higher than conventional vehicles. The batteries used have shorter lives compared to regular vehicles leading to increased maintenance and replacement costs. Opportunity: Rising environmental concerns and stringent government regulations regarding vehicular emissions are driving the demand for fuel-efficient and low-emission vehicles. Growing consumer awareness about fuel-efficient technologies also provides major opportunities for market growth. Threats: Advancements in plug-in hybrid and battery electric vehicles pose a threat. Declining crude oil prices may reduce consumer incentive to purchase hybrid vehicles. Key Takeaways Global Mild Hybrid Vehicle Market Demand is expected to witness high growth, exhibiting CAGR of 18% over the forecast period, due to increasing environmental concerns and stringent emission regulations imposed by various governments and regulatory bodies on vehicular emissions. Tougher Corporate Average Fuel Economy (CAFE) standards and green initiatives by various governments to curb carbon emissions are fueling the demand for fuel-efficient and low-emission vehicles. Regional analysis: Asia Pacific dominated the global mild hybrid vehicle market in 2023, accounting for around 35% share of the overall market revenue. China dominates the regional market owing to the large production volumes of mild hybrid vehicles and presence of key market players such as Toyota and Honda. Europe is another major region for mild hybrid vehicles due to stringent emission norms and tax incentives for purchasing green vehicles by various European governments. Key players operating in the mild hybrid vehicle market are Toyota Motor Corporation, Nissan Motor Co. Ltd, Honda Motor Company Ltd, Hyundai Motor Company, Kia Motors Corporation, Suzuki Motor Corporation, Daimler AG, Volvo Group, Volkswagen Group, BMW AG, Ford Motor Company, Audi AG, Jaguar Land Rover Ltd, Chevrolet. The key players are focused on developing advanced mild hybrid technology and integrating them into their vehicle fleets to comply with emission regulations. OEMs are also investing in manufacturing facilities to cater to the growing demand. Read More- https://www.trendingwebwire.com/mild-hybrid-vehicle-market-value-insights-and-forecast/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed