Glutaraldehyde Market Glutaraldehyde is an organic compound that is widely used as a sterilizing or disinfecting agent. It is commonly used as a high-level disinfectant and cold sterilant for heat-sensitive medical and dental equipment. Glutaraldehyde provides many advantages over other sterilants such as better material compatibility, low temperature activity, and broad-spectrum efficacy. It is commonly used for disinfecting endoscopes, arthroscopes, and other heat-sensitive medical instruments. The global Glutaraldehyde Market is estimated to be valued at US$ 698.4 million in 2024 and is expected to exhibit a CAGR of 4.7% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the Glutaraldehyde Market are Universal Preserv-A-Chem Inc. (UPICHEM), Grassland Agro, Advanced Sterilization Products (Cilag GmbH International), Whiteley Corporation, Sisco Research Laboratories Pvt. Ltd., Lenntech B.V., The Dow Chemical Company, Hubei Jinghong Chemical Co., Ltd., and Evans Vanodine International PLC. Glutaraldehyde Market Demand is expected to witness significant growth due to increasing demand from hospitals and diagnostic centers. The rising number of surgical procedures and growing awareness about hospital-acquired infections are fueling the demand for disinfectants including glutaraldehyde. Technological advancements in the production process of glutaraldehyde are also supporting the market growth. Manufacturers are focusing on developing new production technologies to lower production costs and reduce environmental footprint. Market Trends Growing application of glutaraldehyde in animal health care - Glutaraldehyde is widely used for disinfection purposes in veterinary clinics and animal farms. The rising income levels and growing animal welfare spending are augmenting the demand. Increasing R&D towards developing bio-based glutaraldehyde - With growing environmental regulations, manufacturers are investing in R&D to develop bio-based and eco-friendly alternatives to petroleum-based glutaraldehyde. Market Opportunities Expansion in emerging economies - Emerging regions such as Asia Pacific and Latin America are expected to witness rapid infrastructure development and increasing expenditure on healthcare and animal welfare. This will create new opportunities for glutaraldehyde manufacturers. Glutaraldehyde-based combinations - Combining glutaraldehyde with other stabilizers and neutralizers can help develop enhanced formulations with better disinfection efficacies. This can open new growth avenues. Impact of COVID-19 on Glutaraldehyde Market Growth The outbreak of COVID-19 pandemic has significantly impacted the growth of Glutaraldehyde Market. During the initial lockdown phases across various countries, the production and supply chain of glutaraldehyde were disrupted due to restrictions on transportation and halted activities at manufacturing units. This led to shortage of glutaraldehyde supply which adversely affected its demand from end use industries like hospitals and pharmaceuticals. As glutaraldehyde is prominently used as a sterilant and disinfectant, its demand surged exponentially from healthcare sector during the peak of pandemic. However, the disrupted supply was unable to cope up with the spike in demand. With gradual lifting of lockdowns and resumption of industrial activities, the Glutaraldehyde Market is recovering fast. The manufacturers are ramping up their production capacities to fulfill the growing need of glutaraldehyde from healthcare sector. It is expected that the pandemic will further propel the glutaraldehyde demand in coming years due to increased focus on sterilization and disinfection practices across industries. The long term prospects of Glutaraldehyde Market remain positive driven by growing health awareness post COVID-19. Geographical Regions with Highest Concentration in Glutaraldehyde Market North America region holds the largest share in terms of value in Glutaraldehyde Market, followed by Europe and Asia Pacific. The high market concentration in these regions can be attributed to presence of developed healthcare infrastructure and stringent sterility regulations. In North America, United States represents the major consumer of glutaraldehyde owing to significant healthcare spending and large number of hospitals and medical device manufacturers. Likewise, countries like Germany, United Kingdom and France contribute majorly to Europe's glutaraldehyde demand. The Asia Pacific region is emerging as the fastest growing market with China and India at its forefront due to escalating healthcare expenditures, increasing medical tourism and rising focus on hospital-acquired infection control. Fastest Growing Region in Glutaraldehyde Market Asia Pacific region is poised to accelerate the fastest in Glutaraldehyde Market during the forecast period. This is ascribed to surging population healthcare needs, expanding med-tech industry, growing pharmaceutical manufacturing and rapid establishment of healthcare facilities in emerging countries of the region. Additionally, the rising per capita income, availability of low cost medical services and promotion of health and hygiene by regional governments are driving the market growth. Especially, the Chinese and Indian Glutaraldehyde Markets are witnessing double digit growth led by economic development, urbanization, increasing accessibility and rising standards of living. The growing medical tourism along with governmental initiatives for public health awareness have been propelling the Asia Pacific glutaraldehyde demand. Get More Insights on Glutaraldehyde Market

0 Comments

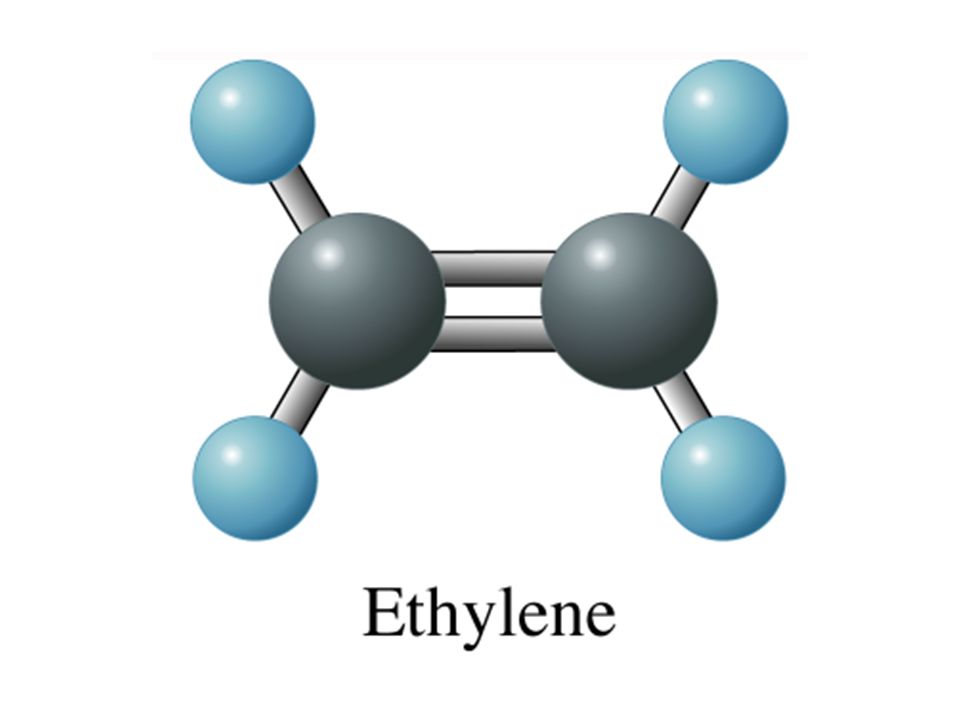

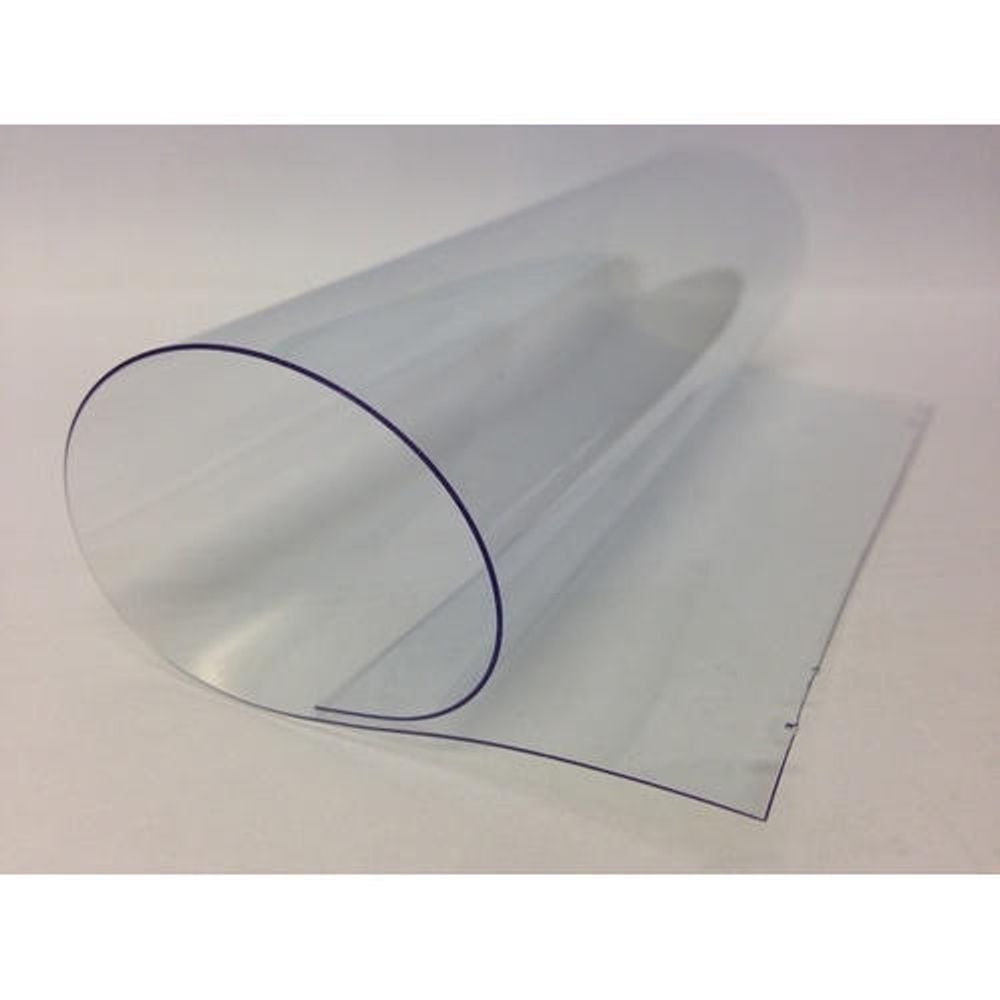

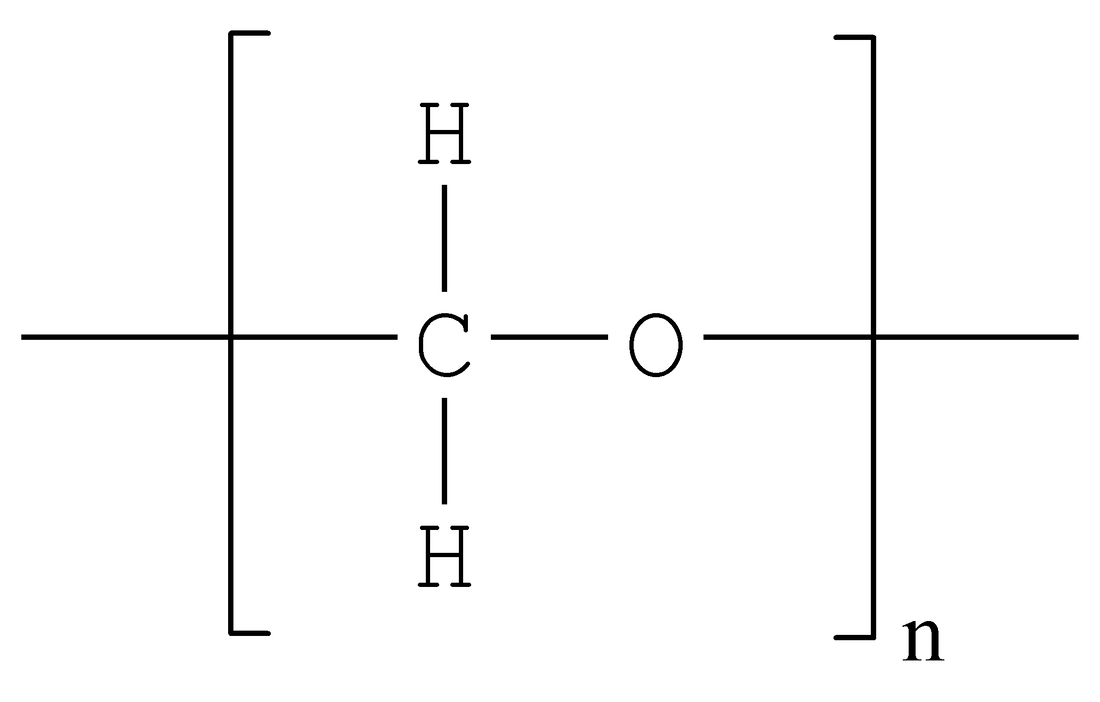

Granular Urea Market Granular urea is an important nitrogen fertilizer used across the agriculture sector owing to its high nutritional content and availability. Granular urea contains 46% nitrogen, which is readily available to plants and helps boost crop growth and yields substantially. It has become one of the most widely used nitrogen fertilizers globally due to its low cost and stable nitrogen content. The agriculture sector has been witnessing significant growth over the years to meet the rising global food demand. This, along with government incentives and subsidies, has increased the application of granular urea fertilizers for various crops such as cereals, grains, fruits & vegetables. The global granular urea market is estimated to be valued at US$ 47.18 Bn in 2024 and is expected to exhibit a CAGR of 13.% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity The rising application in the agriculture sector presents a major growth opportunity for the granular urea market. Population expansion has increased global food demand exponentially. To meet this demand, agricultural production needs to be boosted significantly, which will require higher fertilizer application. Granular urea is one of the most effective nitrogen fertilizers for boosting crop yields. With conducive government policies and subsidy programs in major agriculturally focused countries, granular urea application is expected to rise substantially. This growing demand from the agriculture sector will drive the market over the forecast period. Porter's Analysis Threat of new entrants: The threat of new entrants in the granular urea market is low due to presence of large established players and high capital requirements. However, new players can enter with innovative technology. Bargaining power of buyers: The bargaining power of buyers is high due to availability of substitute products. Buyers can switch to alternative nitrogen fertilizers if pricing is not competitive. Bargaining power of suppliers: The bargaining power of suppliers is moderate as raw materials for granular urea production such as natural gas are available from few large suppliers globally. Threat of new substitutes: The threat of substitutes is high as crop farmers and agriculture industry have alternative nitrogen fertilizer options available. Competitive rivalry: The competitive rivalry in the market is high owing to presence of global producers aiming to strengthen their market position. SWOT Analysis Strength: Granular urea offers highest nitrogen content among N fertilizers. It has uniform distribution and is easily spreadable for even application on fields. Weakness: Granular urea is vulnerable to weather conditions and surface application leads to nitrogen losses. Its misuse can harm soil quality over long term use. Opportunity: Rising population is increasing demand for food which will drive usage of granular urea for improved crop yield. Emerging economies offer growth prospects. Threats: Volatility in raw material prices poses risks. Stringent environment regulations can restrict misuse affecting market. Key Takeaways Granular Urea Market Size was valued at US$ 47.18 Bn in 2024 and is anticipated to grow at a CAGR of 13% during the forecast period. Rising population has increased demand for food which is supporting the consumption of granular urea as nitrogen fertilizer for high crop yields. Regional analysis for granular urea market is dominated by Asia Pacific region led by India and China. Majority of the world's urea production and consumption is accounted by these two countries. Favorable government policies and initiatives to promote fertilizer usage is fueling market growth. North America and Europe are other prominent regional markets growing at steady pace. Key players operating in the granular urea market are Thales Group, Infineon Technologies AG, Ingenico Group, Wirecard, VeriFone, Inc., Giesecke+Devrient GmbH, IDEMIA, Track Innovations LTD., Identiv, Inc., CPI Card Group Inc., Setomatic Systems, Valitor, PAX, PINPAD, Mobeewave, alcineo, and Paycor, Inc. Major players are focusing on capacity expansion plans, new product launches and mergers & acquisitions for strengthening their market position and cater growing demand globally. Get More Insights on this Topic- https://www.rapidwebwire.com/granular-urea-market-value-insights-and-forecast/  Polyphenylene Sulfide (PPS) Market Polyphenylene sulfide (PPS) is a high-performance thermoplastic that is highly stable and resistant to various chemicals and heat. It is majorly used in automotive, electronics & electrical, and filter bags and industrial applications. PPS products are employed in various components in vehicles including electrical components, air intake manifolds, and oil pans. The global increase in automotive production is expected to propel the demand for PPS over the coming years. The global Polyphenylene Sulfide (PPS) Market is estimated to be valued at US$ 1.3 Bn or Mn in 2023 and is expected to exhibit a CAGR of 6.5% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: Increased adoption in automotive sector is one of the major drivers propelling the growth of the global PPS market. PPS exhibits properties like heat resistance, low smoke emission, and chemical & corrosion resistance which make it suitable for use in various automotive components that operate under extreme conditions. Its lightweight properties also help reduce the overall weight of vehicles. Moreover, growing production of electric vehicles worldwide is further augmenting market growth as PPS finds application in battery cases, insulation materials, and charging ports in EVs. However, availability of substitute materials may hamper the market growth during the forecast period. SWOT Analysis Strength: PPS possesses high heat and chemical resistance which makes it suitable for applications in electrical and electronics, automotive, and industrial sectors. The material provides protection against corrosion, insulation, and durability. Its melt flowability enables easy molding through injection molding. Weakness: PPS has high production costs compared to other engineering thermoplastics like polyether ether ketone and polyphenylene ether which limits its use in low-cost applications. The material also has low elongation and poor impact strength which hampers its use in applications requiring flexibility. Opportunity: Growing demand for lightweight and high-performance materials from the automotive industry offers opportunities for PPS market. Increasing focus on fuel-efficient vehicles drives the need for advanced plastics like PPS that help reduce vehicle weight. Rising electrical and electronics consumption globally increases the need for insulation materials having high heat and chemical resistance. Threats: Volatility in raw material prices due to supply chain disruptions can increase PPS production costs, limiting profit margins. Presence of substitute materials like PEEK and PPE that offer similar properties at lower costs threatens the market. Key Takeaways The global polyphenylene sulfide (PPS) market is expected to witness high growth over the forecast period. Global Polyphenylene Sulfide (PPS) Market Size is estimated to be valued at US$ 1.3 Bn or Mn in 2023 and is expected to exhibit a CAGR of 6.5% over the forecast period 2023 to 2030. Asia Pacific dominates the global PPS market and is expected to maintain its leading position during the forecast timeline. China, Japan, India, and South Korea are major consumers as well as producers of PPS resins in the region. The automotive industry accounts for the highest demand for PPS in Asia Pacific attributed to the growing automotive production in developing Asian countries. Key players operating in the polyphenylene sulfide (PPS) market are Toray, Solvay, DIC, Celanese, Tosoh, SK Chemical, Kureha, Chengdu Letian, and Lion Idemitsu. Toray is the global market leader with a significant market share of over 30%. Solvay and DIC are other leading PPS manufacturers having strong presence across major markets. Get More Insights on this Topic- https://www.rapidwebwire.com/polyphenylene-sulfide-pps-market-demand-analysis-and-forecast/  Methylene Chloride Market Methylene chloride, also known as dichloromethane, is an organic compound widely used as a solvent in various industries such as pharmaceuticals, paints & coatings, adhesives, etc. It acts as an excellent solvent for oils, greases, resins, and waxes and is used as a paint stripper and adhesive evaporator. Methylene chloride finds major applications in paint removal, as it easily dissolves road paint and other coatings. It is also employed as an extracting agent in the pharmaceutical industry to obtain valuable chemicals from plant and animal sources. The addition of methylene chloride improves the performance of paints and coatings by improving gloss, flow, leveling, and pigment dispersion. The global methylene chloride market is estimated to be valued at US$ 1.25 Bn in 2023 and is expected to exhibit a CAGR of 10% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: The increasing demand from the paints & coatings industry is estimated to propel the growth of the methylene chloride market over the forecast period. Methylene chloride is widely used as a solvent in paints and coatings formulations owing to its excellent dissolving power. It enhances various properties of paints such as gloss, leveling, flow, and pigment dispersion. The growing construction activities along with an increase in infrastructure development projects across the globe are supporting the growth of the paints & coatings industry. According to the Global Construction 2030 report by Global Construction Perspectives and Oxford Economics, the global construction output is projected to grow by 85% to $15.5 trillion by 2030. This rising demand for paints & coatings from the construction industry will subsequently drive the methylene chloride market growth over the forecast period. SWOT Analysis Strength: Methylene chloride has excellent solvent properties and can dissolve a wide range of materials like paints, lacquers, and varnishes. It evaporates quickly and is non-flammable. These properties have increased its use in various applications. Regulatory approval for specific uses also strengthens demand. Weakness: Stringent regulations regarding methylene chloride usage and exposure limits may restrict growth. It is classified as a probable human carcinogen which raises health concerns. Alternatives are being developed and they pose competition. Production price volatility could dent profits. Opportunity: Demand from emerging economies in Asia Pacific and Latin America is rising due to industrialization. Expanding construction and automotive industries augment the market. New applications in pharmaceuticals and agrochemicals present opportunities. Technology upgrades to produce safer formulations can boost sales. Threats: Regulations banning usage in paint strippers and limiting exposure levels can reduce sales volumes. Customer preference shifting to bio-based and green solvents threatens replacement. Economic uncertainties and demand slowdowns impact the market. Highly competitive landscape keeps pricing and profitability under pressure. Key Takeaways The global methylene chloride market is expected to witness high growth. Global Methylene Chloride Market Size is projected to increase from US$ 1.25 billion in 2024 to US$ 2 billion by 2030, registering a CAGR of 10% during the forecast period. Regional analysis: North America currently holds the highest share owing to stringent implementation of regulations regarding residual VOC content in paints and coatings. However, the Asia Pacific region is anticipated to showcase the fastest growth on account of rising paints, coatings, and adhesive manufacturing. Key players operating in the region are expanding production capacity to cater to the growing demand from end-use industries like construction and automotive. Key players: The key players operating in the methylene chloride market are Dow Chemical, AkzoNobel, Shin-Etsu Chemical Co., Occidental Petroleum, and Solvay. Dow Chemical is one of the leading producers with a global production capacity of over 300kt per year. AkzoNobel is investing in R&D to develop bio-based substitutes to gain market share. Get More Insights on this Topic https://www.marketwebjournal.com/methylene-chloride-market-size-demand-and-share-analysis/ Explore More Trending Articles- https://allmeaninginhindi.com/fiber-reinforced-concrete-the-construction-material-of-future/  Global Ethylene Market Ethylene is an organic compound commonly used as a feedstock in several industrial processes. It is a gas at room temperature and atmospheric pressure. Ethylene has high saturation and is unsaturated in chemical bonds. It has diverse applications as a monomer and intermediate in the chemical and plastics industries. Ethylene is primarily used in the production of polyethylene, which is used to manufacture various plastic products like films, packaging materials, pipes, containers, toys, housewares etc. The global ethylene market size is estimated to be valued at US$ 137.2 Bn in 2023 and is expected to exhibit a CAGR of 9.5% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: One of the key drivers for the growth of the global ethylene market is the increasing demand from the growing plastics industry. Plastics find extensive applications across various end-use industries like packaging, consumer goods, automotive, construction and others. According to Plastic Europe, the global plastic production reached 368 million tonnes in 2020 and is expected to grow further with rising disposable incomes in developing countries. Ethylene acts as the basic raw material for the production of important plastics like polyethylene and polyvinyl chloride (PVC). The growth of the plastics industry in turn drives the demand for ethylene. Another factor fueling the market growth is the increasing use of ethane as a feedstock for producing ethylene. Ethane derived ethylene offers cost advantages and is more environment-friendly compared to naphtha based production. Many companies are investing in building new ethane crackers along ethane pipelines especially in North America to capitalize on the low cost ethane feedstock from shale gas. This shift towards ethane is expected to support the production of ethylene in the coming years. SWOT Analysis Strength: The global ethylene market witness strong growth over the forecast period due to rising demand for polyethylene plastics from packaging industry which accounted for over 50% of global ethylene consumption. Ethylene is also used as a fundamental building block in several important industrial chemicals like ethylene oxide, styrene, vinyl chloride which further boost the market growth. Technological advancements in production processes helps in reducing costs and improving production capacities. Weakness: Intense competition among existing players limits the scope of high profit margins. Supply demand gaps due to unstable raw material prices and geopolitical issues can hamper the steady growth. Stringent environmental regulations regarding emission levels increase compliance costs for manufacturers. Opportunity: Growing demand for ethylene from emerging economies of Asia Pacific due to rapid urbanization and industrialization presents new growth avenues. Rising usage of ethylene in manufacturing of automotive components and equipment expands the application scope. Development of bio-ethylene from renewable feedstock mitigate environmental concerns. Threats: Volatility in crude oil and natural gas prices poses major threat as these are key raw materials. Implementation of alternatives like bio-plastics reduces dependency on petro-based ethylene. Trade wars and geopolitical tensions disrupts global supply chains. Key Takeaways Global Ethylene Market Size is expected to witness high growth over the forecast period supported by rising plastic consumption worldwide. Regional Analysis: Asia Pacific dominates currently with over 50% market share led by China, India and Southeast Asian countries on account of massive polymers and petrochemical industries in the region pleasing the local demand. Countries like China, South korea and India are driving the regional growth at a good pace supported by thriving end use industries and changing lifestyle of consumers demanding packaged and processed food. Key players operating in the global ethylene market are Littelfuse, Inc., RMCIP, Standex Electronics, Inc., Nippon Aleph, HSI Sensing, Inc., Coto Technology USA, PIT-RADWAR S.A., PIC GmbH, STG Germany GmbH, Harbin Electric Group, Zhejiang Xurui, Zippy Technology Corp., Honeywell International Inc., and Molex Incorporated. The market is highly competitive with major focus on capacity expansion, technological advancements and forward/backward integration. Get More Insights on this Topic- https://www.rapidwebwire.com/ethylene-market-demand-forecast-and-outlook/  Transparent Plastics Market Transparent plastics are made from synthetic polymers and are characterized by having transparency up to 90% or more. They find wide application in packaging films, electronic components, automobile components, household appliances, and construction materials due to their properties such as impact resistance, workability, and durability. Transparent plastics such as polycarbonate, acrylic, polymethyl methacrylate, and polystyrene are used to make products ranging from transparent sheets to bottles and medical devices. The global transparent plastics market is estimated to be valued at US$ 167.1 Bn in 2023 and is expected to exhibit a CAGR of 3.6% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: One of the key drivers for the transparent plastics market is the rising demand from the building & construction industry. Transparent plastics have emerged as a preferable substitute for conventional building materials such as glass owing to their lightweight and durable properties. Acrylic and polycarbonate sheets are increasingly being used in roofing, façade construction, greenhouses, and skywalks due to their high optical clarity, weather resistance, and structural strength. Further, the high demand for transparent plastic resins such as acrylic and polycarbonate from end-use industries such as automotive, consumer electronics, and medical is also fueling the market growth. Transparent plastics provide advantages such as transparency, impact strength, durability, and easy manufacturability making them an excellent choice for various industrial applications. However, volatile petroleum prices and increasing environmental regulations regarding non-biodegradability and recyclability of plastics may hamper the market growth during the forecast period. SWOT Analysis Strength: Transparent plastics have superior flexibility and lightweight properties which make them ideal for various applications. They offer durability and withstand harsh conditions. Transparent plastics provide shatter resistance which makes them safer than glass. Weakness: Transparent plastics have lower thermal resistance compared to other materials like glass. Raw material prices for transparent plastics are volatile which impacts the overall production cost. Transportation and disposal of plastic waste raises environmental concerns. Opportunity: Growing construction industry worldwide is expanding the market for transparent plastics in applications like windows, doors, and roofing. Increasing use of transparent plastics in automotive and aerospace industries due to their impact and shatter resistance properties offers new opportunities. Threats: Stringent environmental regulations regarding plastic waste disposal poses a major threat. Population concerns about health impacts of plastic additives can negatively influence the market. Development of new sustainable materials is a threat to replace traditional plastics. Key Takeaways Global Transparent Plastics Market Size is expected to witness high growth. The market size is projected to reach US$ 167.1 Billion in 2023 from US$ 155.2 Billion in 2020, at a CAGR of 3.6% during the forecast period 2023 to 2030. Regional analysis: Asia Pacific dominates the global transparent plastics market currently and is expected to maintain its leading position during the forecast period. Rapid urbanization and industrial development in China and India is driving the demand in the region. North America is another major regional market supported by well-established end-use industries in the US and Canada. Key players: Key players operating in the Transparent Plastics market are Dow Inc., Covestro AG, Eastman Chemical Company, SABIC, Arkema S.A., Mitsubishi Chemical Corporation, Evonik Industries AG, Sumitomo Chemical Co., Ltd., Teijin Limited, LG Chem Ltd. These major players are focusing on new product innovations and geographical expansions to strengthen their market positions. Get More Insights on this Topic- https://www.rapidwebwire.com/transparent-plastics-market-value-insights-overview-and-outlook/  Oil and Gas Descaler Market Oil and gas descaler refers to chemicals used for removal of salts and scale deposits from pipelines, vessels, boilers and heat exchangers in oil & gas industry. Scale deposits hamper heat transfer efficiency and can damage equipment by causing corrosion under insulation. Descalers help clean equipment to restore its thermal efficiency. They find wide application for cleaning of production pipelines, pumps, separators, gas turbines, heat exchangers and other equipment. The global oil and gas descaler market is estimated to be valued at US$ 368.31 Mn in 2023 and is expected to exhibit a CAGR of 10% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: One of the key drivers for the growth of oil and gas descaler market is the increasing investments in exploration activities. According to Oxford Institute of Energy Studies, annual global investments in oil and gas exploration and production are estimated to reach over US$ 481 Bn by 2030. Growing oil rig count and deepwater and ultradeepwater exploration projects indicate higher demand for production and transportation of oil & gas. This increases need for frequent cleaning and maintenance of production assets using descaling chemicals in order to maximize their lifespan. Furthermore, stringent environmental regulations regarding reduction of carbon footprint are also encouraging operators to improve efficiency of existing assets, thereby driving consumption of descalers. SWOT Analysis Strength: The oil and gas descaler market has high demand from the growing oil and gas industry. The oil and gas industry uses descalers to remove hard water scale from industrial equipment to increase their lifespan. Descalers help improve productivity and reduce equipment downtime for maintenance. Weakness: Variations in water chemistry across different oilfields make it challenging to develop universally effective descaler formulations. Some areas may have very hard water that requires highly concentrated descalers. Training operators to correctly apply descalers is also important to avoid damaging equipment. Opportunity: Growing oil production in regions with difficult water chemistries increases the scope for specialized high-performance descalers. Developing eco-friendly descaler solutions without hazardous chemicals can boost their adoption. Remote monitoring technologies allow precise descaling only as needed to minimize chemical use. Threats: Stricter environmental norms around wastewater discharge may impact general descaler selection. Alternative techniques like physical water treatment methods pose a threat. Volatility in crude oil prices impacts exploration and production budgets for downstream users. Key Takeaways Global Oil And Gas Descaler Market Size is expected to witness high growth over the forecast period of 2023 to 2030. The growing oil and gas industry requires effective solutions to remove hard water scale deposits from various industrial equipment to improve their operational life. The global oil and gas descaler market is estimated to be valued at US$ 368.31 Mn in 2023 and is expected to exhibit a CAGR of 10% over the forecast period 2023 to 2030. Regional analysis: North America dominates currently due to major shale oil and gas production. The U.S. and Canada account for over 40% market share. Asia Pacific is poised to grow at the fastest pace led by China, India, and Indonesia ramping up energy production. Key players: Key players operating in the oil and gas descaler market include Audio Network Limited, Envato Elements Pty Ltd., Epidemic Sound, Pond5 Inc., Shutterstock, Inc., SoundCloud Ltd., Inmagine Lab Pte Ltd, The Music Bed LLC, Music Vine Limited, Storyblocks.com, Soundsnap, Soundstripe Inc., Bensound, Jamendo, and ProductionHUB, Inc. These companies offer specialized descaling solutions tailored for different oilfield conditions and strive to develop eco-friendly alternatives. Get More Insights on this Topic- https://www.marketwebjournal.com/oil-and-gas-descaling-market-demand-value-analysis/  Magnesium Hydroxide Market Magnesium hydroxide is a white crystalline solid that is odorless and insoluble in water. It is more commonly known as milk of magnesia and is used as an antacid and laxative in medications. Magnesium hydroxide finds extensive applications as a flame retardant in plastics, rubber, and coatings. It is incorporated into polymers to impart flame retardant properties. Some key end use industries of flame retardant magnesium hydroxide include construction, wires & cables, automotive, and electronics. The global Magnesium Hydroxide Market is estimated to be valued at US$ 826.34 Bn in 2023 and is expected to exhibit a CAGR of 8.5% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: One of the key drivers for the growth of the Magnesium Hydroxide Market is the increasing usage of flame retardant applications. Magnesium hydroxide is an effective flame retardant that decomposes at high temperatures releasing water vapors that dilute any combustible gases and help inhibit flame spreading. The growing fire safety regulations across industries such as construction and automotive have increased the demand for flame retardant additives. According to regulations, wires, cables and plastic components used in vehicles and buildings need to pass certain flame tests. This is positively impacting the adoption of magnesium hydroxide. Additionally, the expansion of end use industries such as construction and electronics will further support market growth over the forecast period. SWOT Analysis Strength: Magnesium hydroxide is non-toxic and non-corrosive, giving it wide application potential. It also acts as a fire retardant and helps inhibit rust formation. Its use in construction materials helps improve durability of structures. Weakness: Dependence on raw material prices as magnesium compounds are obtained from seawater or caustic brine evaporation. Transportation of magnesium compounds over long distances increases costs. Opportunity: Growing construction industry worldwide is driving demand for fire retardant materials. Rising metal production is prompting use of magnesium hydroxide as a desulfurizing agent. Development of advanced applications in plastic, rubber, and pharmaceutical sectors can boost market expansion. Threats: Stringent environmental regulations regarding mining and production processes limit industry growth. Substitutes like aluminum hydroxide and calcium hydroxide pose competition. Economic slowdowns negatively impact end-use industries where magnesium hydroxide is consumed. Key Takeaways Global Magnesium Hydroxide Market Size is expected to witness high growth. Regional analysis related content comprises North America holds the largest share in the global Magnesium Hydroxide Market owing to rapid industrialization and growth in construction industry in the region. Asia Pacific region is expected to witness highest growth rate during forecast period due to expanding manufacturing sector and urbanization in countries like China and India. Key players operating in the Magnesium Hydroxide Market are Sims Metal Management Ltd., Schnitzer Steel Industries, Inc., Nucor Corporation, European Metal Recycling Ltd., Kuusakoski Group, Novelis Inc., OmniSource Corporation, Ferrous Processing & Trading Co. (FTP), Metal Management Inc., ELG Haniel Group. The major players are focusing on expanding their presence in developing economies to leverage potential growth opportunities. Partnerships and mergers with local players help achieve operational synergies. Get More Insights on this Topic- https://www.marketwebjournal.com/magnesium-hydroxide-market-demand-analysis-and-outlook/  Polysilicon Market Polysilicon is a high-purity form of silicon, which is used to manufacture solar PV cells. It acts as the main raw material in the production of solar photovoltaic modules. Polysilicon is used in the production of solar wafers, which are further processed into solar PV cells that convert sunlight into electricity. Growing demand for renewable energy sources and stringent regulations regarding carbon emissions is driving the demand for solar PV modules, thus boosting the growth of the polysilicon market. The polysilicon market is estimated to be valued at US$ 12.80 Bn in 2023 and is expected to exhibit a CAGR of 13% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: The polysilicon market is primarily driven by the increasing demand for solar photovoltaic cells from the solar power industry. Rapid expansion of solar power industry across both developed and developing countries is augmenting the demand for polysilicon. According to International Energy Agency (IEA), global solar PV capacity expanded by 15% per year on average between 2015 and 2019 and reached around 620 gigawatts by the end of 2019. The growth in the market is also propelled by various government policies and initiatives to expand renewable energy sources along with declining costs of solar power generation. However, highly volatile prices of polysilicon owing to fluctuations in supply and demand remains a major challenge for market players. Key players are focused on capacity expansion and R&D activities to reduce production costs. SWOT Analysis Strength: Polysilicon is one of the primary raw material in manufacturing of solar photovoltaic cells. It is abundantly available raw material that can easily be extracted from sand and purified for commercial use. It has long lifespan of over 25 years and minimal maintenance requirement. It provides clean energy and helps reduce carbon emissions. Weakness: Production of polysilicon is a highly energy intensive process requiring high temperature for manufacturing. This makes polysilicon production a costly affair. Supply chain disruptions due to geopolitical issues can impact steady supply of polysilicon. Opportunity: Increasing focus on developing renewable energy resources to reduce dependence on fossil fuels among nations provides growth opportunity for polysilicon market. Government incentives and policies supporting use of solar PV projects drive the demand for polysilicon. Threats: Volatility in prices of key raw materials like trichlorosilane increases the production cost. Dumping of low cost polysilicon from China in the global market impacts competitiveness of other regional players. Key Takeaways Global Polysilicon Market Demand is expected to witness high growth, exhibiting CAGR of 13% over the forecast period, due to increasing focus on renewable energy generation. Regional analysis: China dominates the global polysilicon market with over 50% share due to presence of leading polysilicon manufacturers. Emerging economies of Southeast Asian nations are also fetching lucrative growth opportunities owing to conducive government policies. Key players: Key players operating in the polysilicon market are Sichuan Yongxiang Co. Ltd (Tongwei Co. Ltd), GCL-TECH, DaqoNew Energy Co. Ltd, Wacker Chemie AG, and XinteEnergy Co. Ltd. These players are investing in capacity expansion to cater growing demand for solar grade polysilicon. Get More Insights on this Topic- https://www.rapidwebwire.com/polysilicon-market-share-size-growth-analysis/ Paraformaldehyde is Estimated To Witness High Growth Owing To Its Rising Application in Resins12/11/2023  Paraformaldehyde Market Paraformaldehyde is a thermoplastic phenol-formaldehyde resin which is used in various end-use industries including agrochemicals, construction, pharmaceuticals, coatings, dyes, textiles, and paper. It has various uses as a preservative and sterilizing agent in pharmaceuticals, disinfectants, and vaccines. It is also used in resins, wood adhesives, coatings, and lubricant additives. The Paraformaldehyde market is estimated to be valued at US$ 419.8 Mn in 2023 and is expected to exhibit a CAGR of 3.8% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: The Paraformaldehyde market is primarily driven by its rising application in resins such as phenol-formaldehyde resin (PF resin) and urea-formaldehyde resin (UF resin) for manufacturing particleboards and paper products. These resins exhibit moisture resistance and heat stability which increases their application in particleboards. Additionally, paraformaldehyde is also used in manufacturing coatings due to its hardening and film forming properties. The growing construction industry is augmenting the demand for particleboards and coatings which is further contributing to the market growth. However, stringent regulations regarding formaldehyde emissions is restraining the market growth. SWOT Analysis Strength: Paraformaldehyde has high chemical stability and can withstand high temperatures without decomposing, which makes it suitable for many industrial applications.It has good disinfecting and preservative properties. It is widely used as a fixative in medical applications and cell/tissue preservation. Weakness: Paraformaldehyde produces an unpleasant smell during handling and use. Strict safety guidelines have to be followed during manufacturing and transportation due to its flammable and toxic nature. Opportunity: Growing demand from end-use industries like construction, paints and coatings is expected to drive market growth. Increasing spending on healthcare infrastructure in developing countries also provides new opportunities. Threats: Stringent environment regulations around the world regarding VOC emissions can hamper market growth. Rise in raw material prices is a major challenge. Substitute products also pose a threat. Key Takeaways Global Paraformaldehyde Market Size is expected to witness high growth, exhibiting CAGR of 3.8% over the forecast period, due to increasing demand from various end use industries like construction, paints and coatings. Regional analysis: Asia Pacific region dominated the global market in 2023, accounting for around 36% of the overall shares, owing to high demand from industries in countries like China and India. The region is expected to continue its dominance during the forecast period due to rapid industrialization and infrastructure development activities in developing economies. Key players: Key players operating in the paraformaldehyde market are Ercros, CCP, Celanese, LCY Chemical, Nantong Jiangtian, Hebei Jintaida Chemical, Shangdong Aldehyde Chemical, Yinhe Chemical, Shouguang Xudong, LINYI TAIER, Merck, Mitsubishi Gas Chemical, Chemanol, Xiangrui Chemical, Caldic etc. Get More Insights on this Topic- https://www.rapidwebwire.com/paraformaldehyde-market-growth-insights-and-future-trends/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed